Auto refinancing using personal loans can be a smart financial move for individuals looking to save money and improve their overall financial situation. By refinancing their auto loan with a personal loan, borrowers can take advantage of several benefits that can lead to significant savings in the long run.

One of the primary advantages of auto refinance using personal loans is the potential for lower interest rates. Personal loans often come with lower interest rates compared to auto loans, especially if the borrower has a good credit score. By refinancing their auto loan with a personal loan, borrowers can secure a lower interest rate, which can result in substantial savings over the life of the loan. Lower interest rates mean lower monthly payments, allowing borrowers to free up some of their monthly budget for other expenses or savings.

Another advantage of auto refinance using personal loans is the opportunity to extend the loan term. If a borrower is struggling with high monthly payments on their current auto loan, refinancing with a personal loan can provide them with the option to extend the loan term. By spreading out the payments over a longer period, borrowers can reduce their monthly payment amount, making it more manageable and easing their financial burden. This can be particularly beneficial for individuals facing unexpected financial challenges or those looking to improve their cash flow.

Additionally, auto refinance using personal loans can provide borrowers with the flexibility to consolidate their debts. If a borrower has multiple high-interest loans or credit card debts, refinancing their auto loan with a personal loan can allow them to consolidate all their debts into a single loan. This consolidation simplifies the repayment process by combining multiple payments into one, making it easier to manage and potentially reducing the overall interest paid. It can also help borrowers improve their credit score by reducing their credit utilization ratio, which is an important factor in determining creditworthiness.

Furthermore, auto refinance using personal loans can offer borrowers the opportunity to access additional funds. If a borrower needs extra cash for various purposes, such as home improvements, debt consolidation, or emergency expenses, refinancing their auto loan with a personal loan can provide them with the necessary funds. This option allows borrowers to tap into the equity they have built in their vehicle and use it to cover their financial needs. By leveraging their vehicle’s value, borrowers can secure a personal loan with favorable terms and interest rates, avoiding the need for high-interest credit cards or other costly borrowing options.

In conclusion, auto refinance using personal loans presents several advantages for borrowers. From lower interest rates and extended loan terms to debt consolidation and access to additional funds, refinancing an auto loan with a personal loan can lead to significant financial savings and improved financial flexibility. By taking advantage of these benefits, borrowers can better manage their finances, reduce their monthly payments, and potentially save money in the long run. If you are considering refinancing your auto loan, exploring the option of a personal loan can be a wise decision that may positively impact your overall financial well-being.

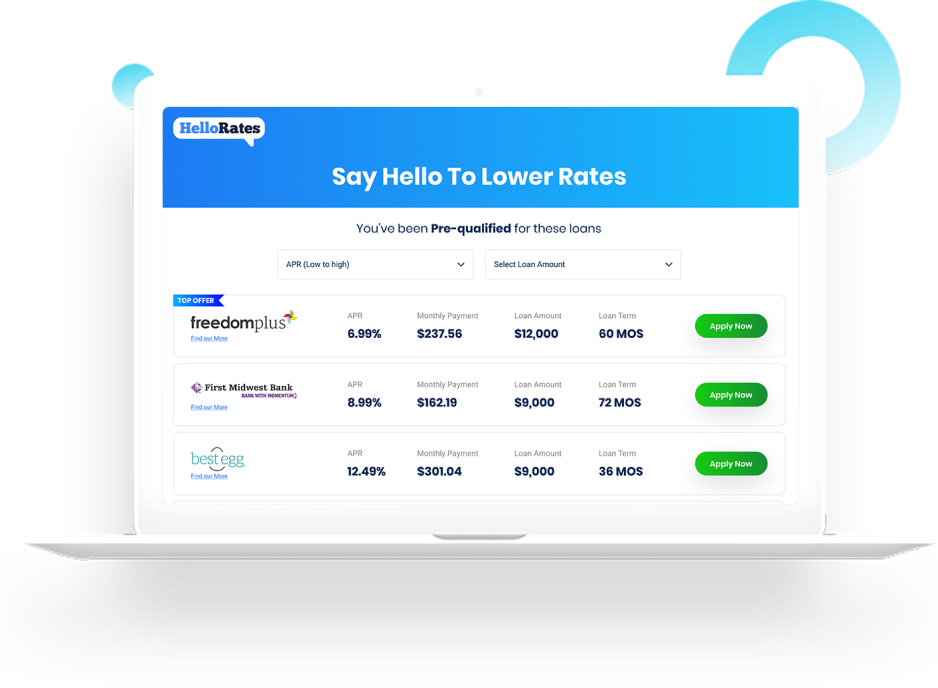

Increase sales by up to 63%

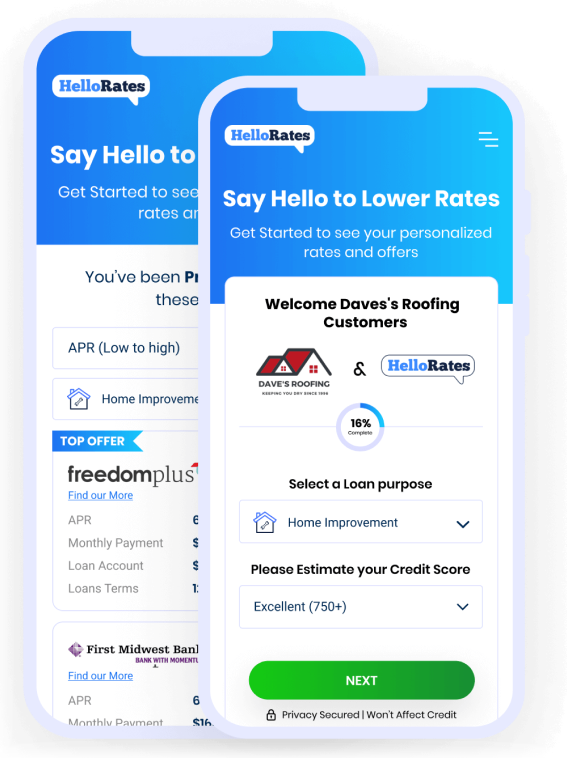

Increase sales by up to 63%