Lumber sales financing through personal loans offers numerous advantages for individuals looking to invest in the lumber industry. Whether you are a contractor, builder, or simply a homeowner planning a renovation project, this financing option can provide the necessary funds to purchase lumber and other building materials. Personal loans are a popular choice due to their flexibility, ease of access, and competitive interest rates. In this article, we will explore the advantages of lumber sales financing using personal loans, highlighting how it can benefit both businesses and individuals alike.

One of the primary advantages of lumber sales financing through personal loans is the flexibility it offers. Unlike traditional financing options, personal loans do not restrict the use of funds to specific purposes. This means that borrowers have the freedom to allocate the loan amount towards purchasing lumber, as well as other related expenses such as tools, equipment, or labor costs. This flexibility allows individuals to tailor their financing to their specific needs, ensuring they have the necessary resources to complete their projects successfully.

Another advantage of lumber sales financing using personal loans is the ease of access. Personal loans are widely available from various financial institutions, including banks, credit unions, and online lenders. The application process is typically straightforward, requiring basic personal and financial information. Many lenders offer online applications, making it convenient for borrowers to apply from the comfort of their homes or offices. Additionally, personal loans often have quick approval times, allowing borrowers to access the funds they need promptly.

Competitive interest rates are yet another advantage of lumber sales financing through personal loans. Personal loans generally offer lower interest rates compared to credit cards or other forms of unsecured financing. This can result in significant savings over the loan term, especially for larger lumber purchases. Additionally, personal loans often come with fixed interest rates, providing borrowers with predictable monthly payments. This stability allows for better budgeting and financial planning, ensuring that borrowers can comfortably repay the loan without unexpected fluctuations in interest rates.

Lumber sales financing using personal loans also offers the advantage of potential tax benefits. In some cases, the interest paid on personal loans used for business purposes, such as purchasing lumber for construction projects, may be tax-deductible. This can provide additional savings for businesses and individuals, reducing their overall tax liability. However, it is essential to consult with a tax professional to understand the specific tax implications and eligibility criteria for deducting personal loan interest.

Furthermore, lumber sales financing through personal loans can help individuals build or improve their credit scores. Timely repayment of personal loans demonstrates responsible financial behavior and can positively impact credit scores. As a result, borrowers may qualify for better loan terms and interest rates in the future. This can be particularly beneficial for contractors or builders who rely on financing for their ongoing projects, as a good credit score can open doors to more favorable financing options and larger credit limits.

In conclusion, lumber sales financing using personal loans offers several advantages for individuals and businesses in need of funds for purchasing lumber and related materials. The flexibility, ease of access, competitive interest rates, potential tax benefits, and credit-building opportunities make personal loans an attractive financing option. Whether you are a contractor looking to complete a construction project or a homeowner planning a renovation, exploring the benefits of lumber sales financing through personal loans can help you make informed financial decisions and achieve your goals efficiently.

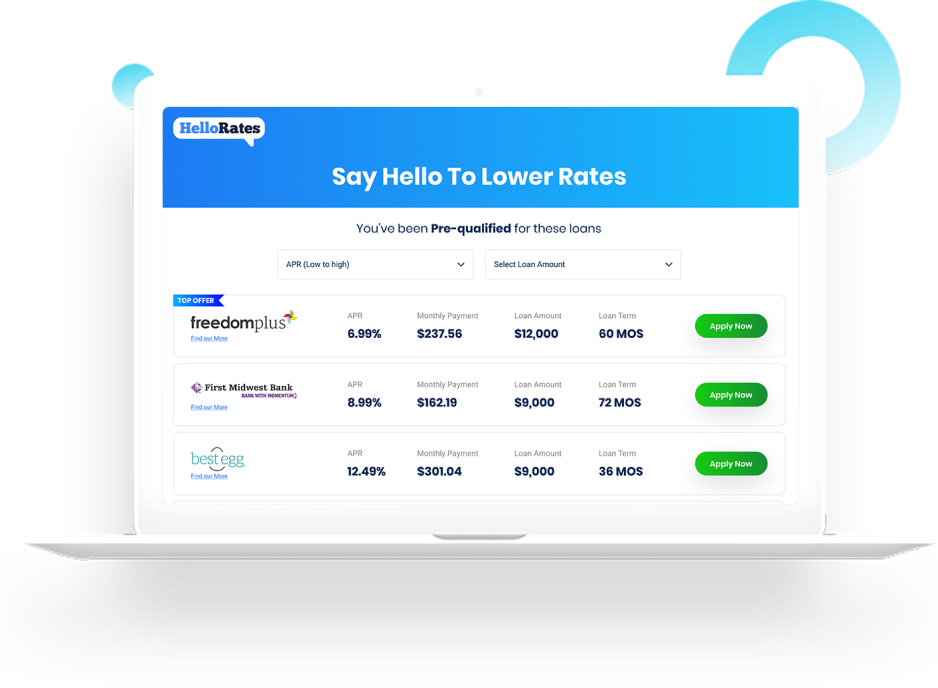

Increase sales by up to 63%

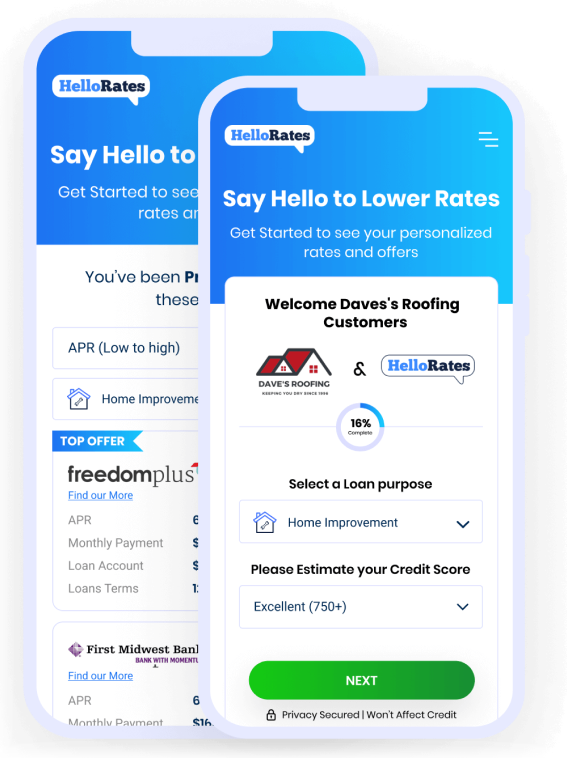

Increase sales by up to 63%