Windows are an essential part of any home, providing natural light, ventilation, and aesthetic appeal. However, replacing or upgrading windows can be a significant investment. To overcome this financial hurdle, many homeowners turn to personal loans as a viable financing option. In this article, we will explore the advantages of using personal loans for windows financing, highlighting the flexibility, accessibility, and cost-effectiveness they offer.

One of the key advantages of financing windows through personal loans is the flexibility they provide. Unlike specific home improvement loans, personal loans can be used for a variety of purposes, including window replacement or upgrades. This flexibility allows homeowners to address other pressing financial needs simultaneously, such as covering unexpected expenses or consolidating high-interest debts. By opting for a personal loan, homeowners gain the freedom to allocate funds as they see fit, making it a versatile financing option.

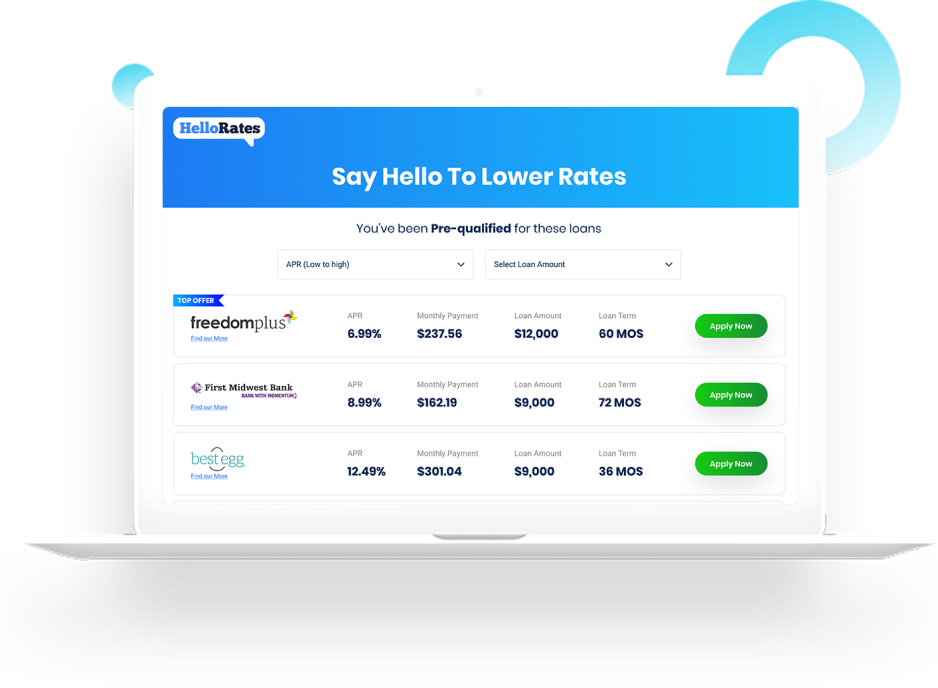

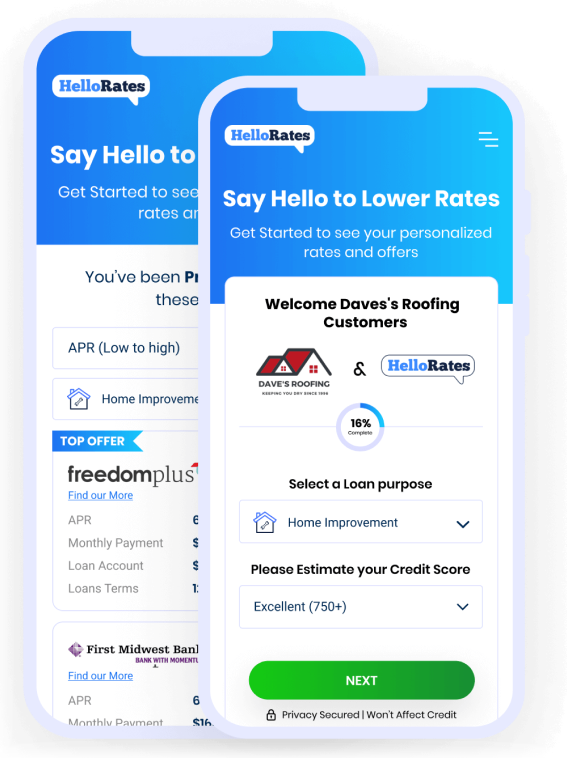

Accessibility is another significant advantage of using personal loans for windows financing. Traditional home improvement loans often require extensive paperwork, collateral, and a lengthy approval process. In contrast, personal loans are typically more accessible, with streamlined application procedures and faster approval times. Many financial institutions and online lenders offer personal loans, making it easier for homeowners to find competitive interest rates and repayment terms that suit their needs. This accessibility ensures that homeowners can quickly secure the funds necessary for their window projects without unnecessary delays.

Cost-effectiveness is a crucial consideration when financing windows, and personal loans can offer significant savings. Personal loans often come with lower interest rates compared to credit cards or other forms of unsecured borrowing. By securing a personal loan with a favorable interest rate, homeowners can reduce the overall cost of financing their windows. Additionally, personal loans usually have fixed interest rates, providing predictability and stability in monthly payments. This allows homeowners to budget effectively and avoid any unexpected increases in interest rates over time.

Furthermore, personal loans for windows financing offer the advantage of spreading the cost over a longer period. Window replacement or upgrades can be a substantial expense, and not everyone has the means to pay for it upfront. Personal loans allow homeowners to divide the cost into manageable monthly installments, making it easier to fit within their budget. This extended repayment period ensures that homeowners can enjoy the benefits of new windows without straining their finances or sacrificing other essential expenses.

In addition to the financial advantages, personal loans for windows financing can also have positive implications for homeowners’ credit scores. When used responsibly, personal loans can help build or improve credit history. By making timely payments and successfully repaying the loan, homeowners demonstrate their creditworthiness to lenders, which can lead to better credit scores. A higher credit score can open doors to more favorable loan terms and lower interest rates in the future, providing long-term financial benefits beyond the immediate window financing.

In conclusion, personal loans offer numerous advantages for homeowners seeking to finance their window replacement or upgrades. The flexibility, accessibility, and cost-effectiveness of personal loans make them an attractive option for those looking to improve their homes without straining their finances. By utilizing personal loans, homeowners can enjoy the benefits of new windows while simultaneously addressing other financial needs. Moreover, personal loans provide an opportunity to build or improve credit scores, paving the way for better financial opportunities in the future. When considering windows financing, personal loans emerge as a practical and advantageous solution for homeowners.

Increase sales by up to 63%

Increase sales by up to 63%